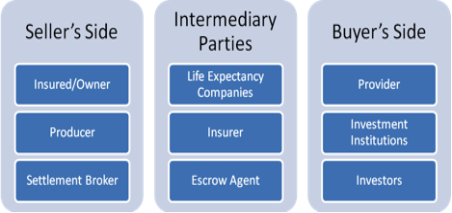

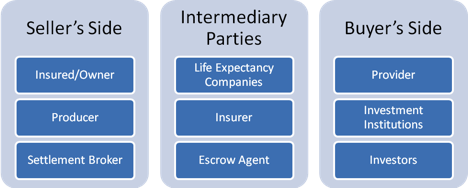

Life settlements are very complex, highly regulated transactions that involve a long process, lots of due diligence, and loads of paperwork. But you can take some of the mystery out of the process if you know the players involved and the part they each play in the process. The process is easier to understand if you grasp that the players fall into three distinct groups: The buyer’s side, the seller’s side, and the intermediary parties.

The Seller’s Side

When a policy owner, with the help of his agent, decides that the policy is going to be cancelled, surrendered or allowed to lapse, the next step is to look for a favorable offer for a life settlement. The seller is the one who initiates the process of obtaining offers for a life settlement. The process, when properly conducted, is always initiated by the seller, not the buyer. A life settlement is not an alternative to keeping a policy, but rather an option to be explored for a policy that is about to be lapsed or surrendered.

Typically, the policy owner’s agent will contact a brokerage that specializes in life settlements. In most states, both the producer/agent and the life settlement brokerage owe a fiduciary duty to the policy owner. They represent the policy owner exclusively and not the buyer. This is in sharp contrast to the relationship in the sale of a new policy, in which an agent, frequently represents the company rather than the prospect, and is rarely held to a fiduciary standard.

Because state laws, regulations, and licensing vary dramatically, it is essential to determine at the outset which state has jurisdiction over the transaction. Generally, it is the domicile of the policy owner, not the insured, which determines the state of jurisdiction. Some life insurance trusts, however, may specify a state that is neither the home state of the insured nor the trustee.

The life settlement broker builds a file for presentation to prospective purchasers. Typically, this process involves obtaining updated in-force ledgers and a 5-years medical history on the insured and the ordering of life expectancy appraisals.

Since the life settlement market is an informal auction market, the life settlement the broker will then solicit interest from potential buyers and try to drive up offers by having them bid against each other. The life settlement broker communicates the offers to the policy owner, who is under no obligation to sell. If an acceptable offer is made, the broker oversees and assists in the completion of the closing paperwork.

The Buyer’s Side

The key players on the buyer’s side of the transaction are the provider, the investment institution and the actual investors. The provider acts as a buyer’s broker and is the primary contact for the seller’s settlement broker.

The provider acts as an aggregator of policies on behalf of one or more investment institutions. Providers acquire policies under several different arrangements. Frequently, the provider has an agreement with an investment institution to acquire policies that meet certain parameters. Other times, the provider identifies attractive policies for purchase and presents them to institutions that are looking to acquire policies. Additionally, much like a builder constructing a home “on spec” a provider might acquire an attractive policy on its own with the hope of reselling it to an investment institution at a future time. Finally, some providers may acquire policies for their own account.

The investment institution might be a bank, investment bank, mutual fund, pension fund, hedge fund, etc. Although the investment institution may be buying on its own behalf, frequently it is representing a group of investors like the shareholders of a mutual fund.

The Provider Versus The Investment Institution

It was once common to use the term “funder” interchangeably to describe either or both the provider and the investment institution. There was a time when the relationship between the two was so close that it felt like they were the same entity. But as the market has matured, the roles of the provider and the investment institution have become more distinct and can no longer be treated as a single party.

The provider does comprehensive due diligence on any policy it has contracted to purchase. The due diligence review seeks to confirm various details about the policy and that the current policy owner has clear title to the policy and the authority to sell it. The review also tries to make certain that the policy was issued to a party with insurable interest and without fraud or misrepresentation.

It is now customary for the investment institution to do its own separate review of the policy. This review is generally done only after the provider has signed off and sometimes additional issues get raised even though the provider has approved the transaction and everybody else thinks it is a done deal.

Intermediaries

The intermediaries also play significant roles in the transaction. Life expectancy companies are independent third parties comprised of doctors, nurses, actuaries, and underwriters that give appraisals of an insured’s life expectancy. Investment institutions frequently require at least two of these independent appraisals before they will allow a provider to make a bid on a policy.

A life settlement is typically, but not always, transacted using the services of an escrow agent (a bank, trust company, or other entity) that holds the policy and the sales proceeds while the closing takes place. Sometimes the escrow agent performs due diligence as well, adding even more time to the process.

The other intermediary, the insurance company, is asked to confirm various details about the policy and its values using a verification of coverage form, or V.O.C.. Next, the insurance company confirms that the ownership and beneficiary of the policy have been changed. These last steps can take several days to a few weeks, and once completed, the escrow company finally releases the proceeds to the seller.

Seats at the Table

As you can see, there are many different players in a life settlement transaction, which makes it a complex, lengthy and sometimes confusing process. The many steps are necessary because of legal requirements to protect the financial interests of investors and policy owners as well as the privacy of the insured. When all is said and done, remember that the policy owner, producer and life settlement broker sit on one side of the table, and the provider, investment institution and investor sit on the other. Understanding these roles and relationships makes the process run more efficiently and ensures that the individual interests of all parties are protected.

{kind=link}

{kind=link}